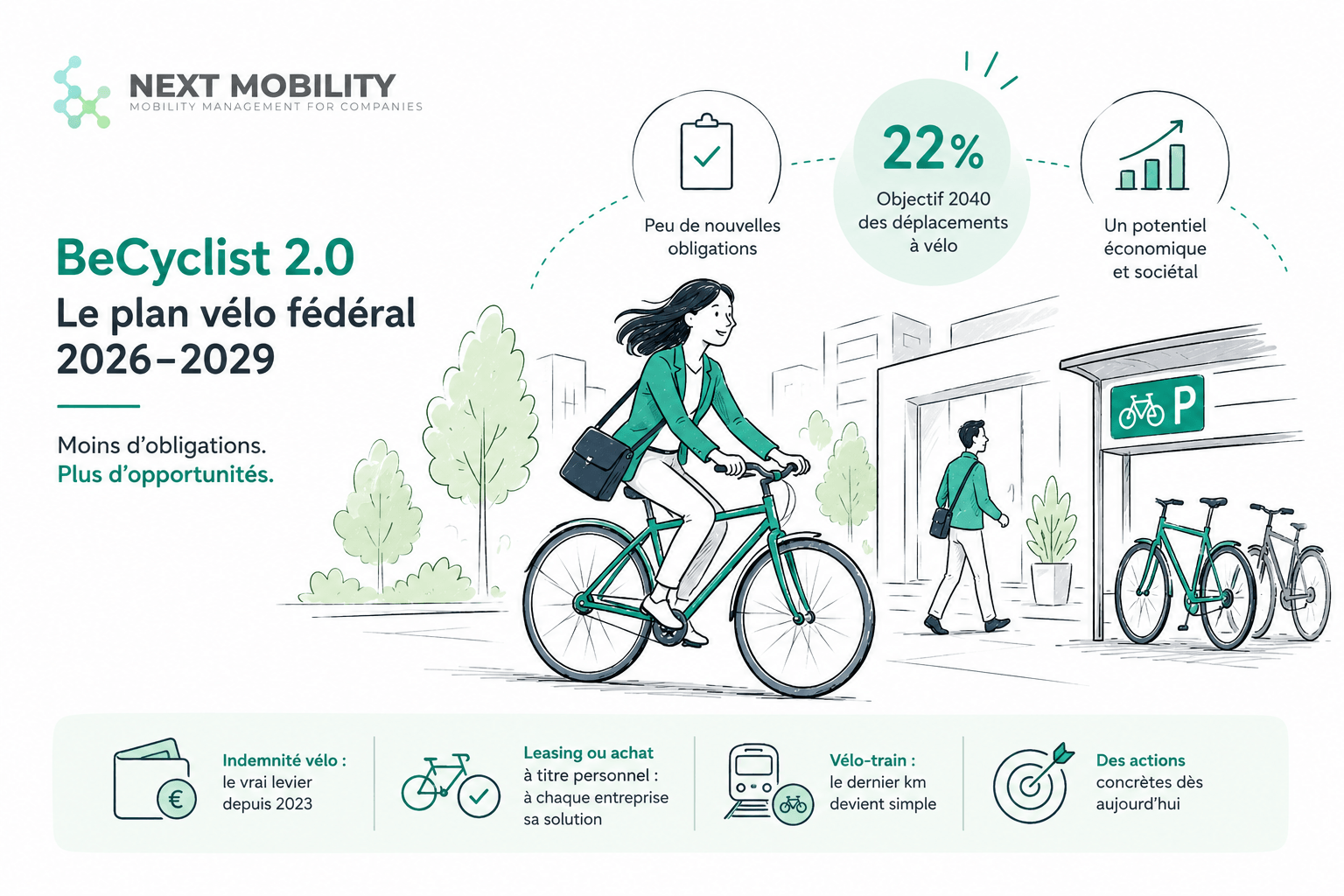

The federal government has approved the “Be Cyclist 2.0” plan, led by Mobility Minister Jean-Luc Crucke. Adopted by the Council of Ministers on 22 May 2026, it extends the first Be Cyclist plan (2021-2024) and covers the period 2026-2029, with targets set for 2040.

Many business leaders will file this under “public policy, not my problem.” A more useful approach is to read it with a simple question: what does it actually change for an employer? The honest answer: fewer new obligations than you might expect, but clear signals about the direction of travel.

The plan in brief

Be Cyclist 2.0 is a federal plan. It activates federal levers — taxation, rail, traffic law, the civil service, public procurement — to support the ambitions of the Regions, which remain responsible for the bulk of cycling infrastructure. It is not an inter-federal plan imposed across the country.

It is built around three strategic axes: making cycling an attractive mobility choice that contributes to modal shift; making it an accessible, safe and healthy mode; and making it an economic driver.

The potential justifies the ambition. Nearly 40% of Belgians’ trip loops are under 5 km, and close to 80% are under 15 km — ideal territory for cycling, especially e-bikes. The quantified 2040 target: raise the cycling share from 12% to 22% of all trips, i.e. from 16 to 28 million kilometres cycled per day. On commuting, the plan notes that Belgium is stuck at 19% of home-to-station trips made by bike (28% in Flanders, 11% in Brussels, 2% in Wallonia), versus 48% in the Netherlands. The gap is considerable.

Few new obligations — and it matters to say so

Let’s be precise, because this is where shortcuts circulate. For a private-sector employer, Be Cyclist 2.0 creates no new immediate obligation. The vast majority of its measures are studies, evaluations or analyses: evaluate bike leasing in the federal civil service (2026-2029), study its roll-out across joint committees (2028), explore a social leasing scheme for low-income workers (2027), budget a reduced VAT rate on bicycle purchases for people with disabilities (2027). These are intentions, not new constraints for your company.

The only real binding lever that already weighs on you has existed for three years: the bike allowance. And it does not come from this plan.

The bike allowance: the real driver, but tracking is the bottleneck

Since 1 May 2023, the bike allowance has been mandatory in the private sector under CLA no. 164 (Collective Labour Agreement no. 164, adopted by the National Labour Council). The plan cites it as an existing achievement, not as one of its own measures — a useful distinction. And the figures it reports speak for themselves: according to the joint report by the Central Economic Council (CCE/CRB) and the National Labour Council (CNT/NAR) of 5 November 2025, 867,751 employees (20.4% of Belgian employees) claimed a bike allowance in 2024, for a total of EUR 329 million, representing a 36% increase in beneficiaries compared to 2021. The same report concludes that the entry into force of CLA no. 164 acted as a catalyst in the positive trend.

But it also highlights wide disparity: in 2025, the amount ranges from EUR 0.15 to EUR 0.36 per km depending on the joint committee, and 20% of those that set a specific allowance attach conditions (daily cap, minimum number of days, maximum distance per trip).

In practice, on the ground, the most common issue I encounter is not a refusal to pay. It is the difficulty of tracking. As long as an employee cycles for 100% of their commutes, it is manageable. The headache begins as soon as there is multimodal or intermodal travel: three days by bike, one day train + bike, one day by car, variable teleworking. How do you declare and verify the kilometres actually cycled without turning payroll into an administrative nightmare? The plan itself implicitly acknowledges this problem: it announces a circular from the FPS Finance (SPF Finances) on the flat-rate VAT deduction for company bicycles with mixed use, precisely to work around “the absence of kilometre tracking.”

The other side deserves equal clarity: once the process is in place, it is a genuine plus for employees. A net benefit, expected, simple to understand. The work is in setting up the tracking correctly from the start.

Leasing: the plan’s big bet — and why I qualify it

The plan’s economic ambition rests heavily on leasing: raising the share of employees with a bike lease from 2.3% to 15%, which would grow this sector from EUR 329 million to EUR 1 billion. The mechanism: a long-term rental (36 months) via the employer, all-inclusive package (insurance, maintenance, roadside assistance), with a buyout at roughly 15% of the value at end of contract, funded from gross salary or the year-end bonus — provided the sector’s CLA allows it, which is not always the case.

It is a common assumption that company cycling equals leasing. That is reductive. In practice, on the ground, within the mobility budget framework, I often advise the opposite: let the employee buy their own bike, or take out a lease in their own name, rather than building a fleet of company bikes. The reasons are operational, not dogmatic. First, no issues when the employee leaves: a personally owned bike leaves with its owner, whereas an employer-sponsored lease requires taking back, buying out or settling the contract. Second, simpler accounting: no contract to depreciate and track per person. Third, lower costs all round, with the employer avoiding the management overhead of a bike fleet.

In this setup, the employer remains central — through the bike allowance and, where applicable, pillar 2 of the mobility budget, which covers bicycle, maintenance and equipment for those who exchange their company car. A caveat, however: when the lease runs through pillar 2, it is fully tax-advantaged, but no exempt bike allowance can be added on top. Leasing retains its relevance in certain cases. It is simply neither the only entry point, nor always the simplest one.

Bike-and-train and parking: the indirect employer link

The plan also banks on the bike-train combination, with a target of 50% of home-to-station trips by bike by 2040 and a commitment from NMBS/SNCB (Belgian Rail) to reach 164,000 bike parking spaces by 2032 (+33,000 compared to 2025). For an employer located near a station, this is a concrete argument to incorporate into a commuting plan: the “last mile” by bike becomes a genuine alternative to the car.

My reading

Be Cyclist 2.0 does not change the game — and that is not a criticism. It is a plan of federal intentions, rich in studies and lean on immediate constraints, that confirms a trajectory forward-thinking employers have already embraced: cycling has become a mainstream daily transport mode, structurally relevant for short trips.

My view is documented and deliberate. In an Avoid-Shift-Improve framework, cycling is one of the most effective levers a company has: for short trips, it avoids the motorised journey altogether rather than making it marginally cleaner. When close to 40% of trips are under 5 km, a bicycle — conventional or electric — is more than adequate for a large share of them, with no parking, no fuel, no marginal cost. This does not hold for everyone: the sales rep covering 200 km a day is not concerned, and a poorly connected or unsafe site changes the equation. But for the majority of short commutes, the question is no longer whether to act. It is how to do it simply, equitably, and measurably — without waiting until 2029.

The Next Mobility approach

This is precisely where we step in. At Next Mobility, we help Belgian employers put these levers into practice — bike allowance and its tracking, the choice between leasing and personal purchase, mobility budget, commuting plan — in a neutral capacity, without selling a proprietary solution, and always grounded in your actual data. The goal is not to add to the burden on your HR or fleet teams, but to lighten it: a clear process, compliant, and accepted by employees.

To benchmark your company against BeCyclist 2.0’s ambitions and identify the two or three highest-impact actions, let’s talk. Our analysis of 20 years of commuting data is a good starting point. Reach us at www.nextmobility.be or directly: nicolas@nextmobility.be.

Sources

- Be Cyclist 2.0 — Federal Action Plan for Cycling 2026-2029, Minister Jean-Luc Crucke, adopted by the Council of Ministers on 22 May 2026 (official press release). Figures cited: 3 strategic axes; 40% of trip loops < 5 km and ~80% < 15 km; 2040 target of 22% of trips by bike (vs ~12%) and 16 to 28 million km/day; bike leasing from 2.3% to 15% of employees (sector EUR 329 million to EUR 1 billion); bike-train 19% in Belgium vs 48% in the Netherlands; 164,000 NMBS/SNCB bike parking spaces by 2032.

- CLA no. 164 (Collective Labour Agreement no. 164, National Labour Council): mandatory bike allowance in the private sector since 1 May 2023.

- Central Economic Council (CCE/CRB) and National Labour Council (CNT/NAR), report on cycling in commuting, 5 November 2025 (CCE/CRB page): 867,751 employees (20.4%) claimed a bike allowance in 2024, EUR 329 million, +36% beneficiaries vs 2021; amounts from EUR 0.15 to EUR 0.36/km in 2025.

- Mobility budget: Act of 17 March 2019 (pillar 2 — sustainable modes).

- Next Mobility analysis: Commuting in Belgium: 20 years of data.