Author: Nicolas Verstraete

~2,300 words · 11-12 min read

Why this FAQ

The official website lebudgetmobilite.be is invaluable. It brings together nearly 150 question-and-answer pairs across 9 sections. It is the legal reference — and we systematically direct people there.

But as of April 2026, it lags behind on three topics that dominate every conversation in companies:

- The 2027 and 2028 obligations. The site itself acknowledges that no official text exists yet: “For now, there is still no official text available concerning the announced changes to the mobility budget…” (Federal Coalition Agreement 2025-2029, p. 39).

- The debate over capping housing costs at €200/month (Renta, FEB) — completely absent.

- Real TCO calculation (EV charging, maintenance, tax treatment 2026-2028) — underdeveloped.

This FAQ covers the 15 questions we hear every month on assignments at Next Mobility. For each one: the short answer, the link to the official fact sheet when it exists, and what we see in practice when the official sources are silent or outdated.

Quarterly updates. If you have a question we’ve missed, write to nicolas@nextmobility.be.

Section A — The 4 framing questions (reformulated)

A1. Who is affected, and from when?

Short answer. The mobility budget exists today on a voluntary basis. It becomes mandatory:

- on 1st January 2027 for companies offering company vehicles to 50+ employees;

- on 1st January 2028 for companies offering company vehicles to 15+ employees.

Official website. The FAQ confirms the current voluntary basis (§2.1) but clarifies: “there is still no official text available” on the obligations announced by the Coalition Agreement.

What we see in practice. The timeline announced by the government is firm enough to structure now. Anticipating avoids last-minute scrambling and is definitely not wasted effort — quite the opposite: a well-designed mobility budget takes 6 to 12 months from diagnosis to first signed policy. If you wait for the official text to start, you’ll miss the deadline.

A2. How is the 50-employee threshold calculated?

Short answer. Based on the average of the last 4 quarters. For an obligation on 1st January 2027, the relevant average will be Q4 2025, Q1 2026, Q2 2026, Q3 2026.

Official website. Not covered.

What we see in practice. This means two things for 2026:

- you know right now whether you’ll be affected in 2027, simply by looking at your DMFA declarations (DMFA (Déclaration Multifonctionnelle / Multifunctionele Aangifte — the quarterly social security declaration submitted by your payroll provider to the NSSO));

- trying to stay under the threshold by manipulating headcount makes no sense: the mobility tools we implement are cost-effective beyond 15 employees.

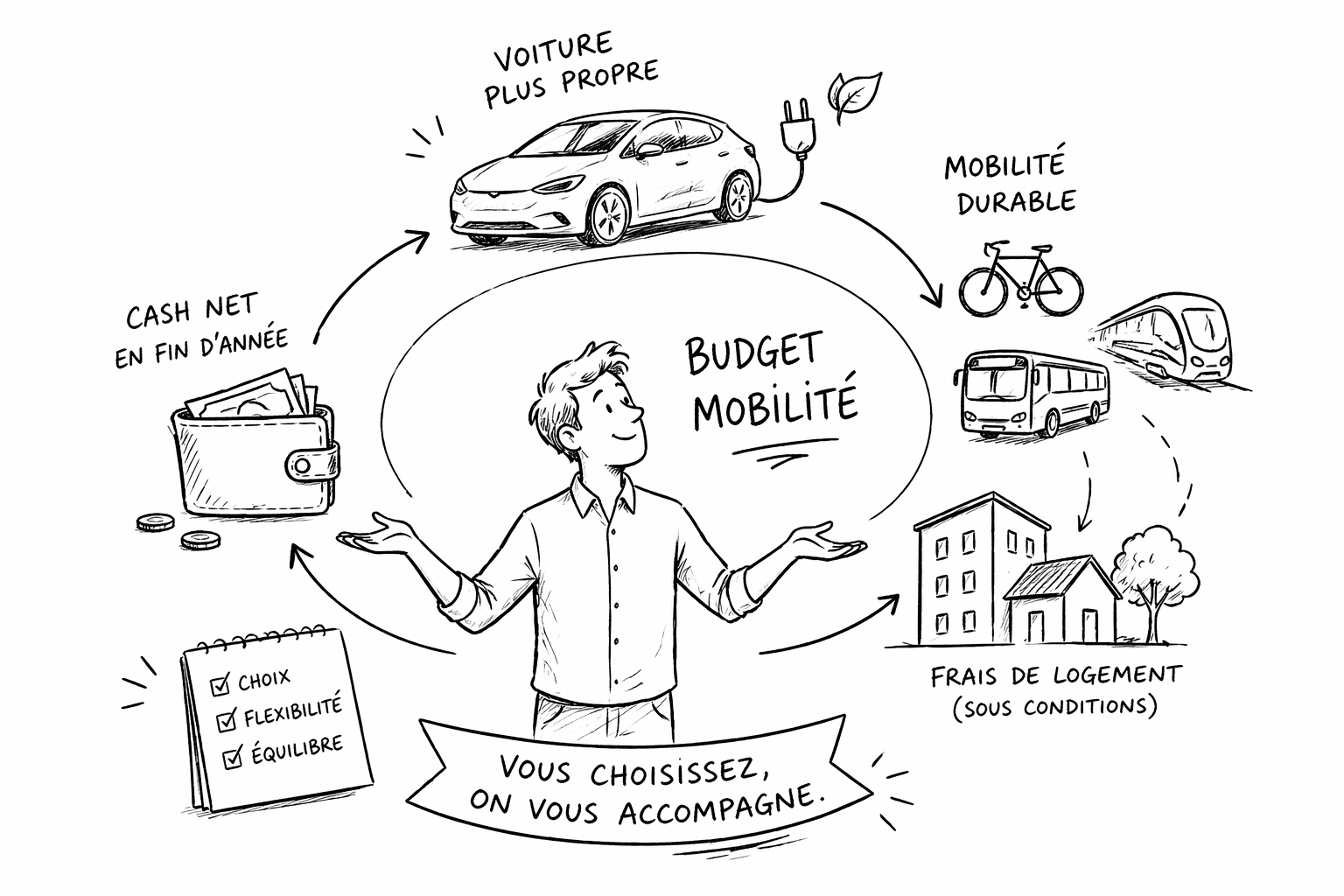

A3. What is a mobility budget, in two sentences?

Short answer. It is an annual envelope, calculated on the total annual cost of the company car (TCO) the employee would otherwise receive, which they can spend freely across three pillars: (1) a cleaner car, (2) a mix of sustainable options (bike, public transport subscription, car sharing, housing costs under conditions), (3) net cash at year-end.

Official website. Detailed in §1 and §5.

What we see in practice. The classic mistake is presenting the mobility budget as “an alternative to the car.” That is not accurate. It is a transformation tool: it allows an employee to choose (and combine) between car, proximity to their workplace, bike, train, and cash — according to their life. Good policy design maximizes rational choices without imposing any particular option.

A4. How much does it cost the employer?

Short answer. The same amount as the employee’s company car — to the euro. The car’s TCO becomes the annual budget with the added certainty of no fuel cost fluctuations if the employee doesn’t choose a car.

Official website. §2.5 and §6 (TCO calculation via Circular 2024_C_16).

What we see in practice. It is cost-neutral for the employer in year 1. It becomes advantageous from year 2 onward:

- less fleet management (tires, accidents, lease exits, claims);

- fewer hidden costs (fuel card, home charging, depreciation);

- lower tax risk (car tax deductibility continues to decline).

The mobility budget rarely costs more. It is an operational simplification dressed up as an HR tool.

Section B — The 7 questions where the official website lags (and what we see in practice)

B1. Should housing costs be capped at €200/month, as Renta proposes?

Short answer. No. Capping at €200/month empties Pillar 2 of all substance. In Brussels, Antwerp, or Ghent, €200 covers nothing. It is a hidden elimination.

Official website. Not covered because this is a position defended by certain stakeholders lobbying in that direction, not an official position.

What we see in practice (full article: “77% of the mobility budget goes to housing. What if that’s exactly what should happen?”)

When 77% of the mobility budget goes to housing costs, it is not a misuse. It is mechanically what the law should produce:

- Distance determines transport mode. The federal survey 2024-2025 proves it: under 5 km, 32% of trips are by bike; over 30 km, cars dominate almost exclusively. Bringing someone closer to their workplace mechanically increases their alternatives.

- When the car is no longer free, behavior shifts. An employee who spends 100% of their budget on housing no longer has a car, no free fuel card, no free leasing. They move rationally: by bike, by train, by rental car when needed. Without constraint, without guilt.

- The money stays in Belgium. Pillar 1: money that goes to Germany, China, South Korea, Czech Republic (carmakers). Pillar 2: rent paid to a Belgian landlord, mortgage in a Belgian bank, renovations by a local contractor — potentially insulation, heat pumps, solar panels.

What really needs correcting is not the cap. It is the “50% telework” exception that allows financing housing 100 km from the office. Keep the 10 km rule. Remove the waiver. Pillar 2 regains its coherence.

B2. Pillar 1 open or closed: what actually changes?

Short answer.

- Pillar 1 closed: the car is outside the budget. The employee has THEIR car or THEIR mobility budget but cannot combine both. Simple, but with no incentive to downgrade.

- Pillar 1 open: the car is within the budget. If I choose a car with €650 TCO and my ceiling is €750, the remaining €100 shifts to Pillar 2 (housing, bike, public transit subscription).

Official website. Not covered.

What we see in practice. Pillar 1 open is the only setup that impacts vehicle choice (and average vehicle size). Without it, the employee takes the biggest car in the catalog (since it is free for them). With it, downsizing becomes a rational choice — they keep the difference for housing or cash. This is the design we recommend systematically.

B3. Bikes and transit subscriptions: can we include household members?

Short answer. Yes. The law allows it.

Official website. Vague in §5.32 and §5.33.

What we see in practice. Including household members (spouse, children living under the same roof) in the Pillar 2 scope for bikes and public transit subscriptions has a double effect:

- direct financial benefit for the employee (a family SNCB subscription, an e-bike for the spouse who also commutes);

- conversational effect at home — mobility becomes a family topic. It is conversations that shift behavior.

This is a lever. Activate it unless you have a reason not to.

B4. Pillar 1 TCO calculation: how do you apply the Circular 2024_C_16 formula in practice?

Short answer. Circular 2024_C_16 offers a theoretically exact formula — but calculated employee by employee. In practice, it is unmanageable: two desk neighbors with the same car would have two different budgets based on their mileage, residence, charging, etc. At Next Mobility, we recommend a flat rate by job category: an average value, stable, communicable, based on reference vehicles.

Official website. Formula referenced in §6, with no guidance on making it operationally viable at company scale.

What we see in practice. The difficulty with the circular is not its content — the formula is sound. It is the level of granularity: applied literally, it requires individual calculation that changes every year with the employee’s profile. No HR manager can manage that.

The solution we use in 9 out of 10 assignments:

- define 3 to 5 job categories (e.g., field team, managers, leadership);

- calculate a flat-rate TCO per category, validated against the Circular as reference;

- update the rate annually, aligned with the car list refresh.

It is easier to communicate, simpler to manage, fairer between employees in the same category. And it is compliant — the Circular does not oppose flat rates; it just provides the underlying calculation method.

B5. If my car list TCO increases this year, must I index the budgets of employees already in the mobility budget?

Short answer. No, it is not required. But we recommend it — to keep the two systems (company car and mobility budget) fair relative to each other.

Official website. Indexation mechanics in §6, but not explicitly addressed.

What we see in practice. If you index the car list every year (logical: inflation and new motorizations raise TCO), but not mobility budgets already assigned, you mechanically create a fairness gap: colleagues on company cars see their TCO rise; those who switched stay on a fixed budget.

Our recommendation: index both annually at the same rate (same percentage as the car list, or inflation). It costs more than a frozen budget, but it eliminates the main complaint heard internally: “people who stayed on the company car come out ahead.” And that is exactly the opposite of the message you want to send.

Decide this in the policy from the start, not after 18 months of grumbling.

B6. Rental cars, taxis, Uber: must they be 100% zero-emission?

Short answer. For regular car-sharing solutions (Cambio, Poppy): yes, 100% zero-emission. For occasional rental (Hertz, Avis for vacations): the law is vaguer. For taxis and Uber: impossible to verify on a standard receipt, and case law has not yet ruled.

Official website. Vague.

What we see in practice. The pragmatic guidance I give my clients:

- regular car-sharing → zero-emission only, that is the spirit of the law;

- occasional rental → tolerance pending clarification;

- taxi/Uber → fundable without specific conditions as long as the invoice says “person transportation.”

B7. An employee refuses the mobility budget. Is that final?

Short answer. The frame is simpler than it seems: an employee cannot truly “refuse” the mobility budget — because you cannot force it on them. It is their choice, voluntary, expressed at specific moments (typically at a car renewal, a new role, or a new hire).

Official website. Implicit in §3, but never stated this clearly.

What we see in practice. The inversion of logic is important: it is not the employee refusing a budget you want to give them. It is the employer proposing an option when the employee must make a choice anyway (lease renewal, transfer, new role). If they say no at that moment, they keep the car. They can say yes at the next opportunity.

Practically, this means two things:

- you need a policy that defines choice moments (end of lease, transfer, hire);

- you need communication tools at those moments (calculator, HR interview, comparison document). This is where most adoptions succeed — or fail.

Section C — The 4 field questions (we hear these every week)

C1. Is Pillar 2 100% deductible for the employer?

Answer. Yes, 100%. And exempt from social contributions and withholding tax for the employee. It’s the most powerful tax advantage of the system — often underestimated.

C2. Does Pillar 1 follow company car tax rules (declining deductibility)?

Answer. Yes. A car chosen in Pillar 1 follows the standard company car tax regime: partial deductibility, ATN, CO₂ contribution. It’s another reason to open Pillar 1 (see B2) — employees understand that staying on a car costs mechanically more over time.

C3. Business mileage: covered by the mobility budget or the employer?

Answer. The rule we apply: align treatment with the company car. If business trips are currently covered by the fuel card (or charging card) of the company car, they are covered by the mobility budget once the employee switches. If your company separately reimburses business travel to employees without a car, you keep that logic.

The goal is neutrality: the coverage method must not depend on the car vs. budget choice, otherwise you artificially make one system more attractive. This point is not addressed on the official website, and it is one of the first questions HR asks when drafting the policy.

C4. An employee already has a car on an active lease. Can they switch to the mobility budget before the lease ends?

Answer. Yes, legally possible if they abandon the company car and pick it back up the next day within the mobility budget. Mechanically: you remove the vehicle from the DMFA (the quarterly NSSO declaration, see A2), move the employee into the budget, and — if they keep the car in Pillar 1 — put it back in the DMFA the next day. It is doable but you need to watch this administrative dance. Many employers prefer to wait for the current lease to end, except in urgent cases.

Summary

| If you… | Then… |

|---|---|

| run a company of 50+ and do not yet have a mobility budget | Start now. The 1st January 2027 deadline is in 8 months. |

| run a company of 15-49 | You have 20 months (deadline 1st January 2028). It goes faster than it seems. |

| are considering capping housing costs at €200 | Read our full article first. You risk gutting the system. |

| do not understand why your TCO comes in higher from one supplier | Ask to see the formula. 9 times out of 10 it is missing charging differences or tax projection. |

| want to test the mobility budget without changing everything | Start with Pillar 1 open on a pilot subgroup (e.g., new hires) — you learn fast and you calibrate. |

Would you rather we handle it?

At Next Mobility, we help Belgian companies set up their mobility budget — from diagnosis to signed policy. Not a 75-page report gathering dust in a drawer: we work on your fleet, your employees, your real operational constraints, and we deliver a policy your HR team can apply the next day.

What makes the difference in our approach:

- we do not sell management tools and we do not push a provider — we help you choose what fits your situation;

- we know the field — we know what holds up 6 months after launch, not just in theory;

- we move fast — a framing workshop and a ready policy in weeks, not months.

📧 nicolas@nextmobility.be · 📅 Book a time slot

Sources

- Official website: lebudgetmobilite.be/fr — Complete FAQ (~150 Q&A)

- Law of 17/03/2019 establishing the mobility budget (amended 25/11/2021)

- Circular 2024_C_16 — Pillar 1 and mobility budget calculation formulas

- Circular 2024_C_19 — mobility budget modifications

- Federal Coalition Agreement 2025-2029, p. 39

- Federal DDT survey 2024-2025 (1.78 million workers)

- Link2fleet articles, March 2026 — housing cost cap debate

- Our article: “77% of the mobility budget goes to housing. What if that’s exactly what should happen?” (March 2026)

Last revision: 23 April 2026 · Next update scheduled: July 2026.

This article is updated quarterly to track changes in the legal framework and sector debates. If an essential question is missing, write to me.